A lot has been said about the Hyflux saga thus far, and if its investors have their say, they would be talking till the cows come home, even if the barn is now empty and the cows have bolted into the sunset.

In fact, there is even going to be a planned protest by retail investors tomorrow at Hong Lim Park, whereby the objective is to appeal to the Public Utilities Board ("PUB") to reconsider its intention to takeover the Tuaspring Desalination Plant ("Tuaspring") at donut.

Well I suppose even Tuaspring can't desalinate any bit of saltiness these investors have. After all, this is an even worse proposition than having potential investor SM Investments ("SMI") come into the picture, where the retail perp and pref shareholders will get a max of 10 cents on the dollar for recovery.

My personal view is that the latest move by PUB is borne out of protecting the country's interest, and it's a great logical move to make. If SMI pushes through their restructuring proposal, it will most likely put forth a restructuring of the economics of Tuaspring with PUB, and having a foreign entity trying to restructure a country's strategic asset with the government would result in a huge landmine of potential undercurrents to traverse through.

It makes absolutely no sense for PUB not to do this, and it seems like they are actually showing some goodwill at taking over Tuaspring at donut, given it seems like they could have contractually asked for Hyflux to pony up the negative net present value of Tuaspring at its current valuation.

As for the timing of PUB's announcement, it's fantastic. Wait till the cards fall, and at the last minute once all information has been gleaned, make your play. Classic, and I can only say bravo.

And if I'm in SMI's position, I would surely walk. A large part of their investment proposal seems to stem on value release on Tuaspring, and with that asset gone, it wouldn't make any sense for me to stay on. For the other assets in the Middle East, I wouldn't quite ascribe them much value if any from a downside credit perspective. Look at the E&Y report for estimated recoveries vs liabilities.

What investors need to know is no one owes them anything. Asking for a backstop for your investment from the government is akin to going to a casino and asking the casino to provide you a guaranteed return on your chips, or a waiver of losses.

One simply does not do that, and no government in its right mind would do something like that, unless of course, it's too big to fail and poses emblematic systemic failure, such as the financial crisis of 2008, where there was a massive bailout of banks and their investors. Even in that situation, one should not expect or ask for something like this to happen.

So how does one prevent a similar situation from happening again? Well, there is no way this can be prevented in a capitalistic society. There will always be business failure, and there will always be a sucker. In this case, the investors (senior banks, retail investors) are unfortunately the suckers. Thus the question is really how can a retail investor prevent oneself from being the sucker.

Here are some tips for the perpetual securities and preferred equity retail investors.

1) Get educated on basic financial and accounting principles

Know what you are investing in and the key business drivers to keep track of to determine viability of holding onto the investment. Look at where you are in the capital structure and the protections afforded to your capital investment.

Hindsight is always 20-20, but to put things in context, in this situation you are quasi equity with no security, loose covenants, and a max 6% unlevered yield. Most likely if Hyflux ends up in insolvency, you'll get donut back, and this should be the operating thesis you'll should be happy to live with.

Also, given the bet of Tuaspring and the revenue contribution of water vs electricity there, if wholesale electricity prices fall on a sustained basis, it'll put the entire project, and the going concern of the Hyflux in jeopardy. Once the price of wholesale electricity falls for a sustained period, one needs to start looking at the viability of the investment.

For the risk-return basis of these perpetual and preferred securities (the "instruments"), I wouldn't have touched them with a ten foot pole. If you didn't quite understand what I had surmised in the above paragraphs, I would kindly suggest to either get educated (there are a lot of accounting 101 courses out there), or to avoid such investments all together.

So lets say you are a yield hog and you like the yield of the instruments, and don't quite understand what Hyflux is doing, and you want to make an investment. In this situation, my suggestion is to de-risk yourself by having a hugely diversified portfolio.

Have no more than 2-3% of your portfolio invested in any investment, and it wouldn't be so painful or necessary to organise nor participate in a useless protest as a method for catharsis.

2) Adopt a skeptical mindset towards anyone trying to sell you investment products

I was a banker in my past life, and specialised in structuring credit loans. Part of my remit involves dealing with private banking clients where we would de-risk ourselves by syndicating some of these credit instruments to ultra high net worth individuals. In these situations, it would always be caveat emptor, buy at your own risk, and there would be big boy letters involved.

From my experience, it isn't that the banker is trying to screw the retail investor, but its that the banker is merely looking out for his own self interest, namely the commission. I can't paint every banker with the same brush, but for one, I wouldn't wake up every morning trying to think of screwing the retail guys, I would just be looking at how to maximise my return on time, namely bonus and commission.

Regardless of the existing regulations at that time, if a banker is trying to sell you an above market yield instrument (6% would surely constitute that) and give you leverage so you can amplify your yield, you should be extremely wary of taking a position on that, more so, even considering taking leverage on that.

You need to do your own homework (see tip #1 above) and come to a conclusion, especially if you are going to sink a majority of your gun powder into it. That said, see tip #1 above again - please diversify and don't take unnecessary concentrated positions to prevent crazy heartache.

As I always preach, in these situations, you can trust, but verify.

And please, don't ascribe blame nor reliance on the auditors in this situation. They were merely doing their gig according to the accounting principles and regulations, and given the drastic changes to the business drivers and hugely levered capital structure, it was pretty obvious that this was a blowout waiting to happen.

Don't hate the game nor the players.

It's one's choice to participate in it, and there are always things one can learn to minimize losses and maximize gains in the future.

Cheers.

Friday, 29 March 2019

Wednesday, 20 March 2019

Expenses - February 2019

| |

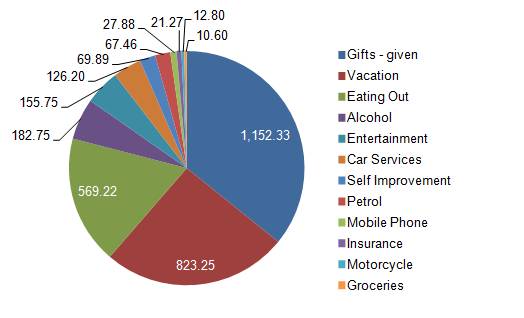

| Total - S$3,219.40 |

Top category was "Gifts - given", which took up c.35% of total monthly expenses. This was attributed largely to CNY as explained above. In addition, my partner's birthday is in February, and we went out to have a nice memorable dinner, plus a useful birthday gift that would hopefully aid her in her practice going forward.

Second largest category was "Vacations", as I cashed out some miles and exchanged some SGD for envisaged spending during my overseas trip come the first half of March 2019.

And third was "Eating Out", as I spent more time outside breaking bread and downing drinks with friends and family during the festive CNY season. Also, this was the first whole month that I was in Singapore, albeit this being a short month, so this category seems just about right.

Total spending came up to S$3,219.40, which is c.19.5% below my monthly budget. Thinking back, this is pretty much the sweet spot, and adjusting for one time expenses such as CNY red packets to parents, it could have been lesser. However, the important thing is that at no time did I feel that I had gone overboard, or that I should be spending less.

It does feel extremely gratifying to be able to have the capacity to deploy resources in exchange for happiness, and this is something I'll always be thankful for.

Subscribe to:

Comments (Atom)